Mike Neary, Manager of Horticulture with Bord Bia, shares findings from a recent Kantar research report into the retail fresh product market.

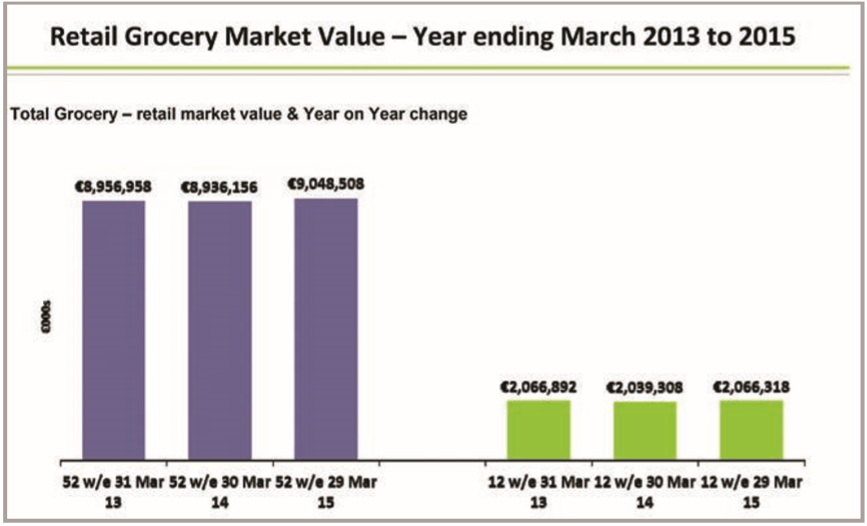

Kantar Worldpanel recently carried a measure of the retail fresh produce market on behalf of Bord Bia. It is the most important market channel for fresh produce. The total grocery market was valued at €9bn in the year ending March 2015. This was a 1.3% increase on the previous year. There was also a corresponding increase in the volume of grocery items purchased over that period.

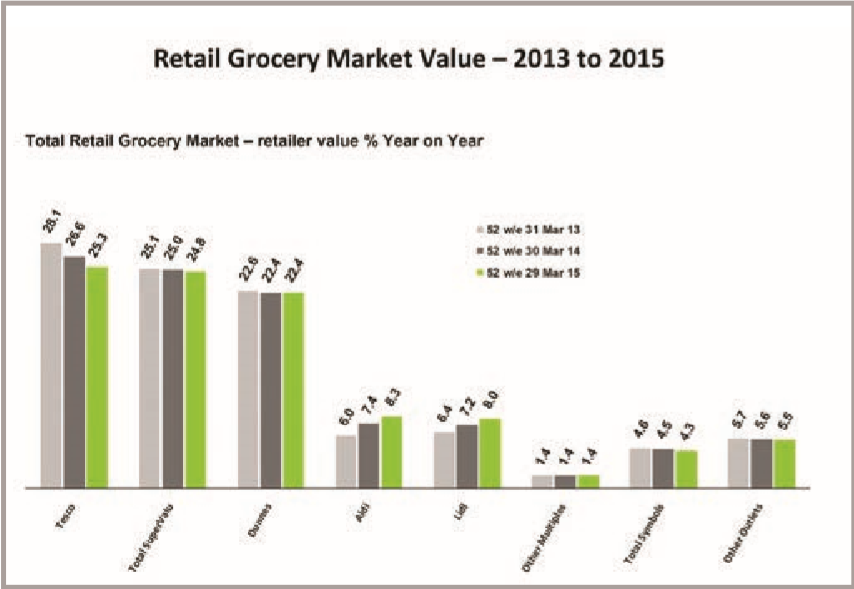

| The major retailers dominate this market channel. Tesco, Dunnes Stores and Supervalu have close to 75% share of the retail market. The discount chains of Aldi and Lidl have a combined share of 16% with the balance of the market shared between other multiples, symbol groups and other outlets. |

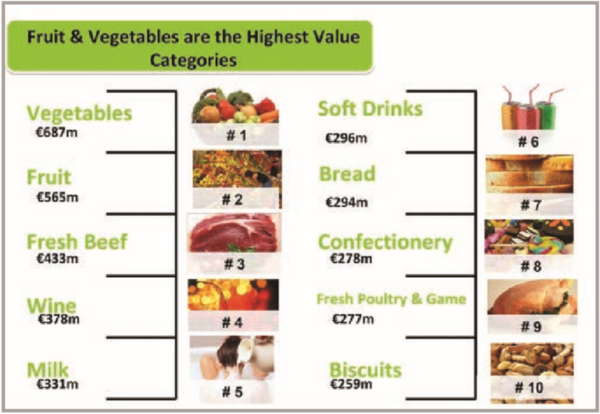

| Fruit and vegetables including potatoes are important purchase items in the weekly shopping basket. In fact, they are the most important, holding the number 1 and 2 positions in value terms across a range of grocery purchase categories making up over 14% of the total grocery spend. |

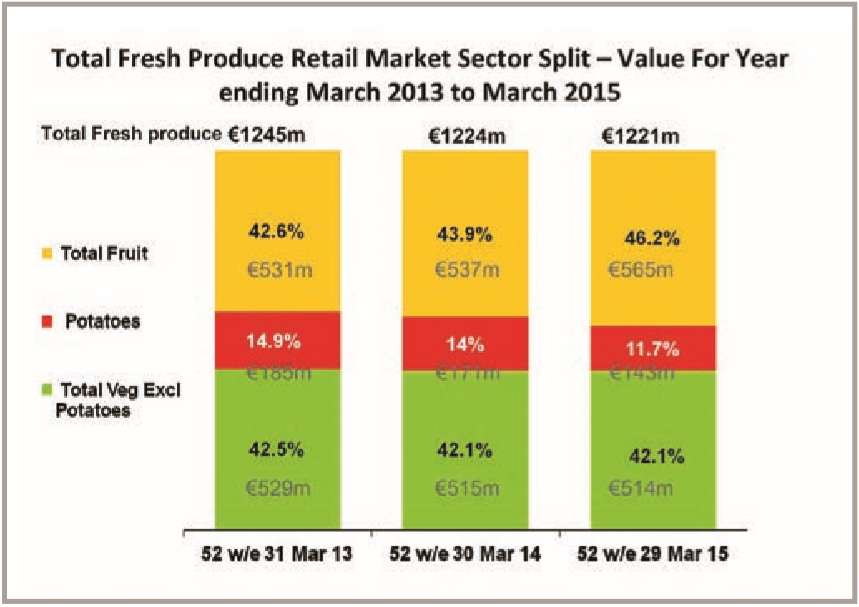

The total fresh produce retail market was valued at €1.2bn in the year ending March 2015. This was a slight decrease of 0.2% on the previous twelve 12 months which was driven primarily by the potato category which saw lower prices at the retail level in the second half of 2014 due to increased supply from increased production area and yields. The fresh produce category comprises the fruit, vegetable and potato categories. These were valued at €565m, €514m and 143m respectively for the year ending March 2015. The value of the fruit category was up while the value of the vegetable category (excluding potatoes) was similar over the previous two years ending March 2014 and March 2015. The purchase frequency for fresh produce was measured at 154 times per year to March 2015 which was up 3% on the previous year. The volume purchased per trip was also up by 3% over the period.

The total fresh produce retail market was valued at €1.2bn in the year ending March 2015. This was a slight decrease of 0.2% on the previous twelve 12 months which was driven primarily by the potato category which saw lower prices at the retail level in the second half of 2014 due to increased supply from increased production area and yields. The fresh produce category comprises the fruit, vegetable and potato categories. These were valued at €565m, €514m and 143m respectively for the year ending March 2015. The value of the fruit category was up while the value of the vegetable category (excluding potatoes) was similar over the previous two years ending March 2014 and March 2015. The purchase frequency for fresh produce was measured at 154 times per year to March 2015 which was up 3% on the previous year. The volume purchased per trip was also up by 3% over the period.

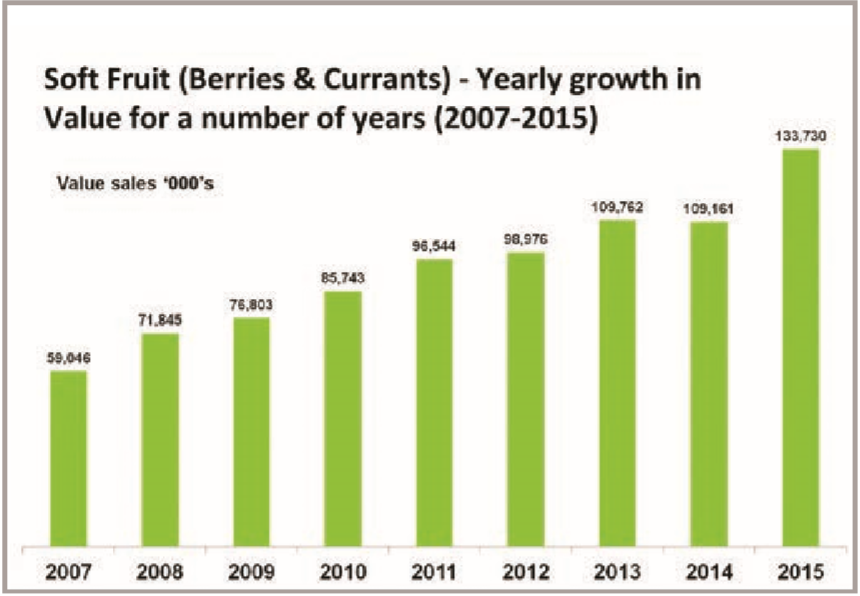

The main fruits grown in Ireland are strawberries and apples. In recent years the growth in the berry and currant category has been dramatic and is currently valued at €133m, of which strawberries are a significant element. Both the volume purchased per buyer and the unit price for the berry category was up in the year ending March 2015. In the apple category, overall spend was back but there was a corresponding increase in volume.

The main fruits grown in Ireland are strawberries and apples. In recent years the growth in the berry and currant category has been dramatic and is currently valued at €133m, of which strawberries are a significant element. Both the volume purchased per buyer and the unit price for the berry category was up in the year ending March 2015. In the apple category, overall spend was back but there was a corresponding increase in volume.

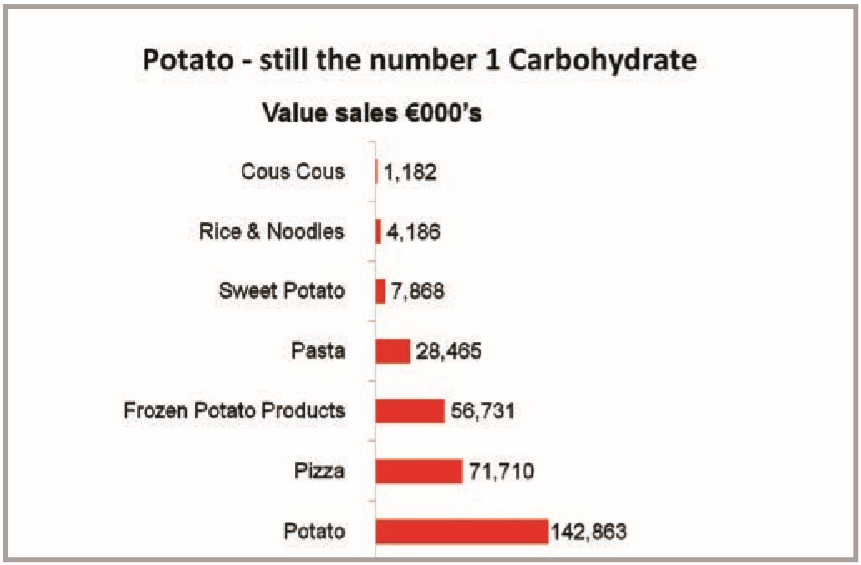

The value of the potato category saw the biggest decline for the year ending March 2015, driven primarily by the volume available to the market. However, this value at the supermarket shelf did result in an increase in the volume of potatoes purchased with the volume purchased per trip up by 10% over the period. Along with an increase of 2% in the frequency of purchase, this resulted in a volume growth over the period of 13% though this was not enough to counteract the decline in the value of the category. Recent years have seen a decline in the consumption of potatoes but nevertheless, it is still the number one source of carbohydrates for Irish households.

The value of the potato category saw the biggest decline for the year ending March 2015, driven primarily by the volume available to the market. However, this value at the supermarket shelf did result in an increase in the volume of potatoes purchased with the volume purchased per trip up by 10% over the period. Along with an increase of 2% in the frequency of purchase, this resulted in a volume growth over the period of 13% though this was not enough to counteract the decline in the value of the category. Recent years have seen a decline in the consumption of potatoes but nevertheless, it is still the number one source of carbohydrates for Irish households.

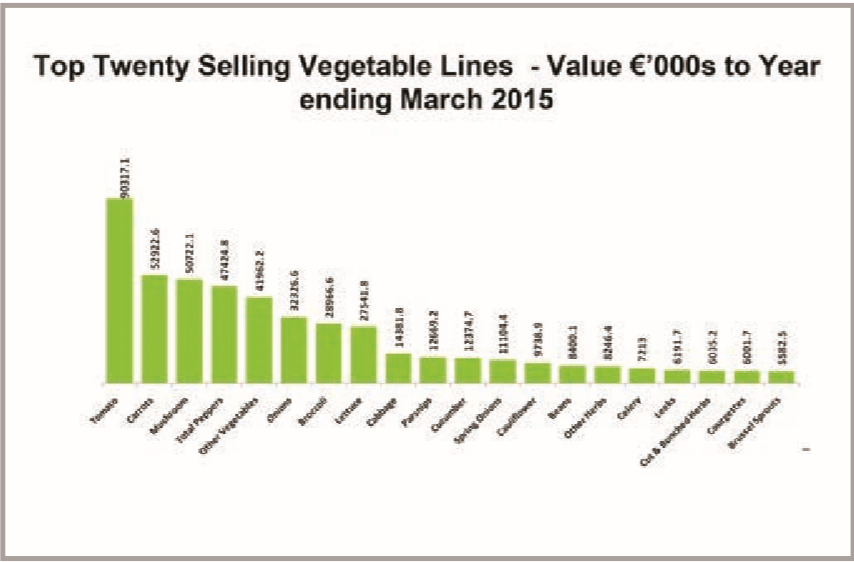

The vegetable category saw an increase in volume sales for the year ending 2015, driven by a lower unit price over the period. The volume increase came from an increase in the frequency of purchase (up 3%) and an increase in the volume purchased per trip (up 2%). Carrots, mushrooms and peppers are the top four contributors to the value of the vegetable category.

The vegetable category saw an increase in volume sales for the year ending 2015, driven by a lower unit price over the period. The volume increase came from an increase in the frequency of purchase (up 3%) and an increase in the volume purchased per trip (up 2%). Carrots, mushrooms and peppers are the top four contributors to the value of the vegetable category.

{kind=link}